Rental income is taxable in Canada and must generally be reported to the CRA each year. However, you are only taxed on your net rental income, not the total rent you collect. This means you can deduct eligible rental expenses before calculating the amount subject to tax.

| Item | Tax Treatment |

| Rent collected from tenants | Taxable income |

| Eligible rental expenses | Deductible |

| Net rental profit | Taxable |

| Rental loss | May offset other income in certain situations |

| Unreported rental income | Can result in penalties and reassessments |

For most property owners, the formula is simple: Rental Income – Eligible Expenses = Taxable Rental Income. Understanding which expenses qualify and how rental income is reported can help you avoid costly mistakes and reduce your overall tax bill.

We provide a full suite of Accounting and Bookkeeping Service in Coquitlam and throughout various areas of British Columbia.

How Is Rental Income Calculated in Canada?

The CRA taxes rental income based on the profit generated by your property.

The basic calculation looks like this:

| Calculation Step | Example |

| Annual rent collected | $30,000 |

| Less eligible expenses | $12,000 |

| Net rental income | $18,000 |

The net amount is added to your other income and taxed at your applicable tax rate.

Rental income can come from:

- Residential rental properties

- Basement suites

- Condominiums

- Vacation properties

- Multi-unit rental buildings

- Commercial rental properties

Even if rent is received in cash, it must still be reported.

Our other tax services:

- Personal Income Tax Return

- Corporate Tax Filing

- Payroll Tax Filing

- WCB Claim Filing Services BC

- ROE Service in Coquitlam

What Rental Expenses Can You Deduct From Your Income?

The CRA allows property owners to deduct reasonable expenses incurred to earn rental income.

Common deductible rental expenses include:

- Property taxes

- Mortgage interest

- Insurance premiums

- Utilities paid by the landlord

- Property management fees

- Advertising expenses

- Accounting and bookkeeping fees

- Repairs and maintenance

- Legal fees related to rental operations

For example, if you collect $25,000 in rent and incur $10,000 in eligible expenses, only the remaining $15,000 would generally be subject to tax.

Not Sure Which Expenses Qualify?

Many landlords either miss legitimate deductions or accidentally claim expenses incorrectly. Reviewing your rental property expenses with a professional can help maximize deductions while ensuring full CRA compliance. MaxPro Financials helps rental property owners across British Columbia identify deductible expenses and maintain accurate records throughout the year.

Is Rental Income Taxed Differently for Individuals and Corporations?

Yes. The tax treatment can differ depending on whether the property is owned personally or through a corporation.

Individual Ownership

Most rental properties are owned personally. In this case:

- Net rental income is reported on the owner’s tax return.

- Income is taxed at personal tax rates.

- Expenses are deducted against rental income.

Corporate Ownership

When a corporation owns the property:

- Rental income is reported on the corporate tax return.

- Different tax rules may apply.

- Corporate tax rates may differ from personal tax rates.

- Additional planning opportunities and complexities can arise.

The best ownership structure depends on factors such as the number of properties owned, long-term investment goals, financing considerations, and overall tax planning objectives.

How Is Rental Income Reported for Jointly Owned Properties?

When a rental property has multiple owners, each owner generally reports their share of the rental income and expenses.

For example:

| Ownership Share | Income Reported |

| 50% ownership | 50% of income and expenses |

| 25% ownership | 25% of income and expenses |

| 75% ownership | 75% of income and expenses |

The allocation should generally reflect the actual ownership arrangement rather than simply splitting income evenly.

Common joint ownership situations include:

- Spouses

- Family members

- Business partners

- Investment groups

Maintaining clear records of ownership percentages can help avoid reporting issues.

Our other financial services:

- Financial Service Coquitlam

- Business Valuation Services BC

- Business Plan Consultants

- Budgeting and Financial Planning

- Financial Due Diligence Services

What Happens If You Do Not Report Rental Income?

Failing to report rental income can create significant problems with the CRA.

Possible consequences include:

Reassessment of Tax Returns

The CRA may reassess prior tax years and add unreported income.

Additional Tax Owing

Taxes that should have been paid originally may become due.

Interest Charges

Interest can accumulate on unpaid balances.

Penalties

Depending on the circumstances, penalties may also apply.

Increased CRA Scrutiny

Repeated reporting issues can increase the likelihood of future reviews.

The CRA receives information from many sources and increasingly uses data matching to identify unreported rental income.

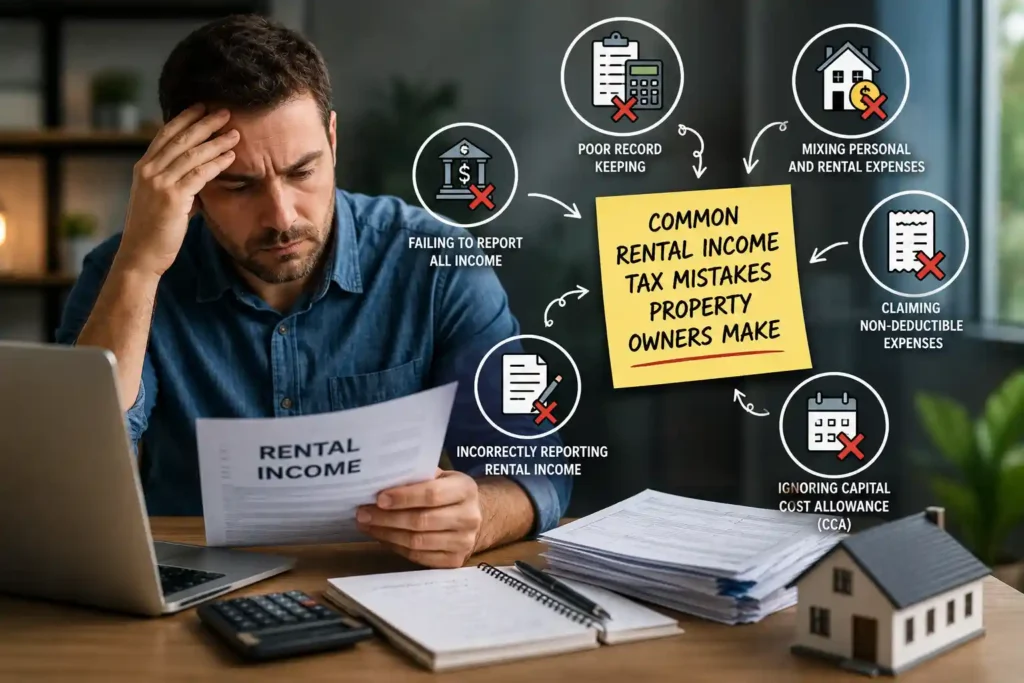

Common Rental Income Tax Mistakes Property Owners Make

Many rental property owners make avoidable mistakes that increase taxes or create CRA issues.

Not Reporting All Rental Income

Even occasional or short-term rental income generally needs to be reported.

Claiming Personal Expenses

Only expenses related to earning rental income can usually be deducted.

Misclassifying Capital Improvements

Major renovations are often treated differently than routine repairs.

Poor Record Keeping

Missing receipts and incomplete records can lead to denied deductions.

Incorrect Ownership Allocation

Joint owners should report income and expenses based on actual ownership interests.

Forgetting Mortgage Principal Is Not Deductible

Only the interest portion of mortgage payments is generally deductible.

These mistakes are common among both new and experienced landlords.

Reduce Rental Property Tax Mistakes and Keep More of Your Investment Income

Owning rental property can be an excellent way to build long-term wealth, but understanding the tax rules is essential. Proper reporting, accurate record keeping, and claiming the right deductions can significantly improve your after-tax return while reducing CRA risks.

At MaxPro Financials, we help rental property owners throughout British Columbia manage rental income reporting, identify deductible expenses, maintain CRA-compliant records, and develop tax-efficient strategies for their real estate investments. Whether you own one rental property or an expanding portfolio, our team can help you stay compliant and keep more of your investment income.

FAQ

Do I have to report rental income if I only rent my property for part of the year?

Yes. Rental income generally needs to be reported regardless of how long the property was rented during the year.

Is a security deposit considered rental income?

Not usually when received. However, amounts retained later for damages or unpaid rent may have different tax implications.

Can rental losses reduce other income?

In some situations, legitimate rental losses may be used to offset other sources of income, subject to CRA rules.

Do I need to report rental income from Airbnb or short-term rentals?

Yes. Income earned through short-term rental platforms is generally taxable and must be reported.

Can I deduct travel costs related to my rental property?

Certain travel expenses may qualify if they are directly related to managing or maintaining the property.

What records should I keep for rental income?

Keep lease agreements, rent receipts, bank records, invoices, expense receipts, mortgage statements, and any documents supporting income and deductions.

Does the CRA receive information about rental income from other sources?

The CRA uses various data sources and matching programs to verify reported income, including information from financial institutions and other organizations.

Should I use an accountant for rental property taxes?

Many landlords benefit from professional advice, especially when dealing with multiple properties, joint ownership arrangements, capital improvements, or complex tax situations.